Doing Business in Türkiye: Legal guide

2025

Norton Rose Fulbright and Pekin Bayar Mizrahi have a professional alliance to provide clients with access to top-tier cross-border consulting and Turkish legal advice. Norton Rose Fulbright’s global network of international lawyers collaborate with Pekin Bayar Mizrahi lawyers to counsel international and domestic clients on complex business transactions covering a variety of issues, including corporate, M&A, securities, banking and finance, capital markets and dispute resolution work.

Norton Rose Fulbright has been active in the Turkish market for more than 25 years and opened its Istanbul office in 2011. Norton Rose Fulbright provides a full scope of legal services to the world’s preeminent corporations and financial institutions. The global law firm has more than 3,000 lawyers advising clients across more than 50 locations worldwide, including Houston, New York, London, Toronto, Mexico City, Hong Kong, Sydney and Johannesburg, covering the United States, Europe, Canada, Latin America, Asia, Australia, Africa and the Middle East. Norton Rose Fulbright ranks first in Chambers Global 2024 for the number of lawyers ranked in global-wide practice areas/categories. The firm is ranked 20th in the 2024 American Lawyer Global 200 and 15th in the Am Law 200.

Norton Rose Fulbright Verein, a Swiss verein, helps coordinate the activities of Norton Rose Fulbright members but does not itself provide legal services to clients. Norton Rose Fulbright has offices in more than 50 cities worldwide, including Istanbul, London, Houston, New York, Toronto, Mexico City, Hong Kong, Sydney and Johannesburg.

Pekin Bayar Mizrahi is one of the oldest and largest law firms in Türkiye. Established in 1946, Pekin Bayar Mizrahi is a full-service law firm that has been advising clients globally on matters of Turkish law for more than 75 years. With approximately 35 lawyers, the firm is led by Selin Bayar and leading disputes partner, Ergin Mizrahi.

Chambers Global 2024 recognizes Pekin Bayar Mizrahi as a leading Corporate/M&A firm in Türkiye, while The Legal 500 Europe, Middle East and Africa 2024 ranks the firm as a leader in Türkiye in the following areas: banking, finance and capital markets; dispute resolution; and commercial, corporate and M&A.

All information in this publication is current as of [January] 2025.

Norton Rose Fulbright extends its thanks to Gamze Şulen and other members of its Istanbul team for their valuable contributions to the preparation of this publication. Pekin Bayar Mizrahi extends its thanks to Aslı Kucuroğlu Alkan, Ceylan Necipoğlu, Deniz Altınay, Duygu Özmen, Ferhat Pekin, Galya Kohen Benbanaste, Hande Alp, Maral Celepyan Avşar, Meral Arabacı, Sertaç Kökenek, Utku Ünver and Senem Gölge Yalçın.

I. INTRODUCTION

A. An Overview: Geography and Population

B. Economic Overview

C. Legal System

II. CORPORATE ENVIRONMENT

A. Corporate Structures

B. Fiduciary Duties

C. Accounting and Audit

D. Minority Rights

E. Termination

III. PROTECTION OF FOREIGN INVESTMENTS

A. Domestic Legislation on Foreign Investment

B. International Treaties

C. International Dispute Resolution

D. Istanbul Arbitration Centre (ISTAC)

IV. PROPERTY RIGHTS

A. Acquisition of Title and Ownership Rights

B. Non-ownership Rights to Property

C. Intellectual Property

V. BANKING AND FINANCE

A. Banks

B. Available Financing Structures

C. Security and Collateral

D. Enforcement of Security Interests

E. Foreign Exchange Control

F. Hedging and Derivatives

G. Costs of Financing

VI. CAPITAL MARKETS

A. Regulatory Framework

B. Securities Offering

C. Trading of Securities

D. Disclosure Requirements

E. Corporate Governance Requirements

F. Crowdfunding

G. Capital Markets Activities

VII. FINANCIAL INSOLVENCY AND RESTRUCTURING

A. Financial restructuring (finansal yeniden yapılandırma)

B. Concordat (konkordato)

C. Bankruptcy (iflas)

D. Restructuring through consensus (uzlaşma yoluyla yeniden yapılandırma)

VIII. ENVIRONMENTAL LAW

A. Sanctions

B. Environmental Permits and Assessments

IX. LABOR LAW

A. Elements of Employment

B. Termination of Employment

C. Subcontracting

D. Transfer of Business by the Employer

E.Unions and Collective Bargaining Agreements

F. Temporary Employment

G. Remote Employment

H. Occupational Health and Safety

I. Employment of Foreigners

J. Turkish Workers in Foreign Countries

X. COMPETITION LAW

A. Prohibited Actions and Exemptions

B. Abuse of a Dominant Position

C. Merger and Acquisition Transactions; Prior Approvals

D. Clearances

E. Investigations and Complaints

XI. ANTI-CORRUPTION

XII. DATA PROTECTION

XIII. ENVIRONMENTAL SOCIAL AND GOVERNANCE (ESG)

XIV. SECTOR HIGHLIGHT I – ENERGY

A. Electricity Market

B. Renewable Energy.

C. Oil and Gas

XV. SECTOR HIGHLIGHT II – MINING

XVI. SECTOR HIGHLIGHT III – INFRASTRUCTURE & PRIVATIZATIONS

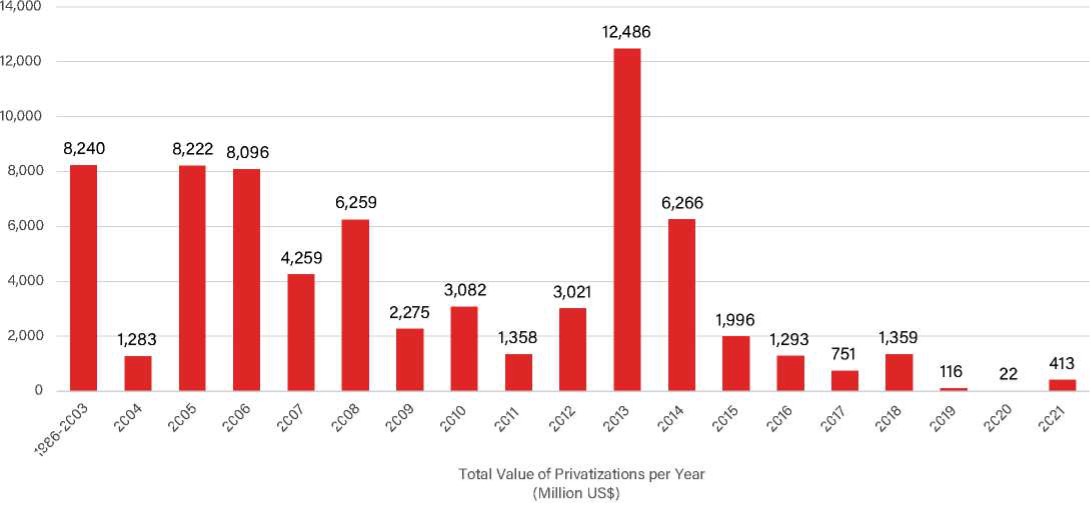

A. Privatization

B. PPP Models

C. Financing of PPP Projects: State Guarantees

XVII. SECTOR HIGHLIGHT IV – FINTECH

A. PAYMENT SERVICES AND E-MONEY INSTITUTIONS

B. DIGITAL BANKING

C. CRYPTO ASSETS

XVIII. SECTOR HIGHLIGHT V – HEALTHCARE

I. INTRODUCTION

A. An Overview: Geography and Population

The Republic of Türkiye is situated at the geographic crossroads of Europe and Asia. Türkiye shares European borders with Greece and Bulgaria and neighbors Syria, Iraq, Iran, Azerbaijan, Armenia and Georgia in Asia. It is surrounded by seas on three sides. The Black Sea forms its northern coastline and links Türkiye with Southeastern Europe, Russia and the Caucasus. The Aegean Sea borders its western coastline and channels through Europe. The Mediterranean Sea borders its southern coastline and ties Türkiye with the Middle East and North Africa.

Türkiye is also positioned at the intersection of strategic trade routes on three continents. Istanbul is a major regional air hub connecting passengers within a four-hour flight radius to capital cities in Europe, Western and Central Asia, the Middle East and Africa.

Türkiye is a member of the OECD, WTO and NATO and has been a European Union accession candidate since 2005.

Türkiye is home to the second largest population in Europe. According to TURKSTAT, the population of Türkiye as of 202 is approximately 85.3 million people. Nearly three-quarters of the population is between the ages 15 to 64, with a median age of 34, 10.5 years younger than that of the European Union.

B. Economic Overview

Introduction

A largely free-market economy with a combination of traditional agriculture, modern industry and a dynamic services sector, Türkiye’s economy is one of the largest in Europe and the MENA region. The World Bank database currently ranks Türkiye as having the 18th highest GDP in the world, as measured according to current US$ value.

Often viewed by investors as having a large skilled and cost-effective workforce, the OECD ranks Türkiye as the 6th largest labor pool in the world and the 3rd largest labor pool among the European countries.

Main Sectors

Agriculture, industry and services are all key components of the Turkish economy, contributing roughly 6.5 percent, 31.87 percent and 52.2 percent, respectively, to the GDP. Manufacturing is driven by strong sectors such as automotive, textile and consumer goods. Türkiye’s automotive industry is the 12th largest producer in the world. The services industry is driven by the financial services, telecommunications, construction, tourism and healthcare sectors. In particular, real estate assets have been a strong target of foreign investment.

Energy

Türkiye’s growing economy and the increasing demand for energy, which cannot be met by the currently available domestic energy resources, has resulted in a dependency on energy imports, primarily oil and gas. According to the International Energy Agency, more than 91 percent of the oil resources and 100 percent of the gas resources used in Türkiye are imported.

In recent years, dependency on fuel imports and environmental concerns have led to a focus on renewable energy sources such as wind, solar and geothermal. In addition, integration of nuclear power into the Turkish energy mix has become a key aspect of the country’s plans for securing the energy demand which is necessary for economic growth. Construction of the first of three planned nuclear power plants – the Akkuyu facility on the Mediterranean coast – began in April 2015 and is still ongoing. In 2023, the energy and natural resources minister announced that Türkiye found natural gas worth more than US$500 billion in the Black Sea.

Liberalization of the energy market, through privatization of production and distribution assets, as well as market deregulation, has created significant investment opportunities in almost all components of the value chain for electricity, natural gas, oil and coal.

Türkiye is a critical energy corridor facilitating the trade of oil and gas between the world’s crucial suppliers in Western Asia and the large consumer market in Europe. Several large pipeline projects are in operation or under development. Of significance are the Baku-Tbilisi-Ceyhan (BTC) crude oil pipeline, which runs from the Caspian Sea to the Mediterranean, passing through Azerbaijan, Georgia and Türkiye; TurkStream, which runs from Russia to Türkiye through the Black Sea; and the Trans-Anatolian Natural Gas Pipeline (TANAP) which runs from Azerbaijan through Türkiye to Europe.

Taxation

There are three general tax categories in Türkiye: income taxes, taxes on wealth and taxes on expenditure. In addition, there are social security contribution requirements for both employers and employees.

Income taxes are applicable to real persons as well as corporations. While the corporate tax rate is flat, personal income tax is levied at progressive rates on an individual’s annual taxable income, the highest rate being 40 percent. The tax rate pertaining to the corporate income (CIT) in Türkiye was set at 25 percent for the 2023 taxation period, however, the CIT rate for financial sector companies is 30 percent. Taxes on wealth include real property tax, motor vehicles tax, inheritance tax and gift tax. Real property tax ranges between 0.3 percent and 1 percent of the registered value of the real property. The rate of motor vehicles tax depends on the age and engine capacity of the vehicle. Inheritance and gift taxes are levied at a rate of 1 percent to 30 percent.

Taxes on expenditures include value added tax (KDV), special consumption tax, stamp tax and banking and insurance transaction tax (BSMV). Unless there is a specific exemption, KDV is levied at a rate that varies between 1 percent and 20 percent on the purchase (including importation) of various goods and services. Special consumption tax applies to the sale of certain goods such as alcohol and tobacco. Please see “Cost of Financing” under “Banking and Finance” for further details on taxes.

Social security contributions are calculated on the basis of monthly wages and are paid jointly by the employer and the employee. Currently, the employer’s share is 22.5 percent (subject to a 5 percentage point decrease, subject to certain conditions) and the employee’s share is 14 percent of monthly gross earnings, including salary and bonuses, where gross earnings are capped at a monthly amount (currently ₺150,018.9).

As part of the social security contributions mentioned above, employers and employees are required to make contributions of 2 percent and 1 percent, respectively, of the employee’s gross salary to the unemployment insurance fund.

Türkiye has several investment incentive programs which provide benefits and exemptions from one or more types of taxes. Eligibility for an incentive program depends upon the scale, geographical location and strategic nature of the investment.

The Parliament is the primary competent authority that imposes, amends and revokes tax obligations. It may also authorize the President to set various tax rates, within the range specified by the relevant tax law. The Ministry of Finance implements tax laws and regulations.

Türkiye is party to double-taxation treaties with many countries. These treaties prevent double taxation and allow cooperation between Türkiye and other applicable tax authorities. For more information on Türkiye’s international treaty commitments, please see “International Treaties” under “Protection of Foreign Investments.

Currency

Türkiye uses a floating exchange rate regime under which exchange rates are determined by supply and demand conditions in the market. Foreign exchange bid prices are published on a daily basis on the Central Bank website.

C. Legal System

Constitutional Structure

The Turkish constitutional structure has operated as a multi-party system for 75 years.

The first constitution of the Republic of Türkiye was adopted in 1924 and the current constitution dates back to 1982. Although Türkiye initially adopted many of its legal codes from Switzerland, France and Italy, in recent years, in conjunction with the country’s European Union accession process, both the Constitution and the legal codes have undergone significant amendments. Please see “Constitutional Amendments of 2017” below for information on the scope of the most recent constitutional amendments.

The Turkish constitutional system is based on the separation of powers. The Constitution provides for a single legislative body, the Parliament, an executive branch comprised of the President and an independent judiciary represented by a multi-layer court system divided into civil, criminal and administrative authorities.

The legislative power of the state is vested in the Parliament, which is comprised of 600 members. Under a closed list electoral system, voters do not cast ballots for candidates but rather for a political party based on a candidate list presented by the political party. Seats in Parliament are proportionally allocated to political parties gaining 10 percent or more of the national electoral vote. Members of the Parliament represent the entire nation and serve five-year, renewable terms. The Parliament is vested with powers to adopt and repeal laws, debate and adopt legislative proposals on the state budget, print money, ratify international treaties and declare war.

The executive branch is the Presidency. The President is elected by direct national vote for a five-year term with the possibility of being re-elected for a second five-year term. The President is the head of state and has the power to veto legislation. A presidential veto may be overridden by the Parliament if a simple majority of its members adopt the proposed law for a second time and without amendment.

The Turkish judiciary is an independent body of the public administrative system. The overarching structure of the judiciary is a multipartite system embodying two distinct court systems: general courts (including civil, commercial, criminal, labor and family courts) and administrative courts. In the general and administrative judiciary, there are courts of first instance, appellate courts (istinaf mahkemeleri) and high courts. The high court of general jurisdiction is the High Court of Appeals (Yargıtay) and the Council of State (Danıştay) is the highest administrative court. The highest court for constitutional review and adjudication is the Constitutional Court of Türkiye (Anayasa Mahkemesi).

Turkish courts’ review of a dispute is focused on establishing the facts of the dispute and applying the provisions of the relevant code to those facts. Both the fact-finding and legal analysis functions are carried out by a judge who, in practice, often appoints expert witnesses to submit reports to the court. There is no jury system. Unlike in common law systems, the role of the judge is limited in terms of law-making. In the absence of an applicable statutory provision, judges may establish applicable rules on a case-by-case basis; however, this authority is rarely used. This authority does not extend to criminal law cases.

As a general rule, court precedents provide non-binding guidance to courts. In other words, the stare decisis principle, emblematic of common law jurisdictions, is less stringently adhered to in Türkiye. However, decisions of the plenary sessions of the High Court of Appeals and the Council of State that address conflicting applications of the law from different chambers (also known as decisions on the unification of conflicting judgments) establish binding precedents.

Constitutional Amendments of 2017

The constitutional amendments, approved through a public referendum held on April 16, 2017, include comprehensive revisions to the Turkish governmental system, replacing the dual-structured executive branch with a presidential system.

The amended Constitution grants broader executive powers to the President through consolidating the authorities of the now defunct Council of Ministers, including those of the Prime Minister, in the President’s office. Subject to certain restrictions, the President has the right to issue presidential decrees (cumhurbaşkanlığı kararnamesi) to undertake activities whose approval is not, for whatever reason, sought from Parliament, such as a unilateral declaration of a state of emergency, a call for early elections or to issue regulations to implement laws. The President also has the right to propose an annual budget to the Parliament. If the Parliament does not ratify the President’s proposed annual budget, it may adopt a provisional budget. Failing passage of a provisional budget, the prior year’s budget, adjusted using a revaluation ratio, automatically becomes law.

Under the amended Constitution, the Council of Ministers has been abolished, and the Parliament no longer has the power to appoint or dismiss any executive officer. Rather, the Parliament may, with the approval of three-fifths of its members, call for early elections. Regardless of the branch of government calling for early elections, simultaneous elections are held for both the Parliament and the Presidency. In the event that Parliament calls an early election during the President’s second term, the incumbent President may be elected again.

The amended Constitution also, among other things, abolished the military judiciary, revised the structure and composition of the Constitutional Court and abolished the concept of by-laws (tüzük) that were, in the past, issued by the Council of Ministers upon review of the Council of State.

Sources of Law

Türkiye is a civil law jurisdiction. The legal system is based on comprehensive legal codes (laws). Duly ratified international treaties also carry the force of law. The provisions of a treaty become applicable when the Parliament enacts a law announcing the entry into force and execution of the relevant treaty.

Below is an explanation of the legal hierarchy under the current Constitution and is intended to be read with the subsection “Constitutional Amendments of 2017” above.

Laws may only be enacted by the Parliament, not by courts. However, since general laws are not always sufficient to accommodate the daily needs of society, administrative authorities are empowered to issue secondary legislation containing more technical, in-depth provisions relating to the implementation of a law.

The legal hierarchy in Türkiye can be stated as follows:

- First, the Constitution;

- Second, international treaties that are duly ratified by the Parliament that concern fundamental rights and freedoms (such as the European Convention on Human Rights);

- Third, statutory laws, presidential decrees and other international treaties duly ratified by the Parliament;

- Fourth, regulations and ministerial communiqués.

Fundamental Laws

Türkiye’s fundamental laws are largely based on other major continental European legal systems. For instance, the Turkish civil law system incorporates elements of Swiss law, Turkish commercial law is largely based on German law, Turkish administrative law bears similarities to French law, and the Turkish criminal code is similar to its Italian counterpart. The fundamental laws (also known as codes) in force in Türkiye are:

- The Civil Code governing the general rules and principles applicable to individuals and legal entities residing or incorporated in Türkiye, as well as their general dealings with each other (such as personal status law or family law);

- The Code of Obligations regulating the rights and obligations (contractual or non-contractual) of private persons vis-a-vis each other;

- The Commercial Code regulating commercial undertakings, companies, negotiable instruments, maritime law and insurance agreements;

- The Labor Law governing the relationship between the employee and the employer;

- The Criminal Code governing general principles of criminal law, various categories of crimes and applicable penalties; and

- Administrative law composed of various laws regulating the functions of governmental bodies and their relationship with individuals and legal entities.

In addition to these fundamental laws, there are non-sectoral laws (such as competition and environmental law) and sectoral laws (such as banking, capital markets and energy) that form an important part of the business landscape. The main regulatory entities with rule-making and implementation authority are the various ministries and separate regulatory agencies created to supervise certain activities, including the BDDK, the Capital Markets Board, EPDK and the Competition Authority. These regulatory agencies are independent, administratively and financially autonomous public institutions.

II. CORPORATE ENVIRONMENT

The main legislation governing the Turkish corporate sphere is the Commercial Code. The current Commercial Code, which came into force in 2012, replaced the prior commercial code that had been in force for over 50 years.

A. Corporate Structures

Legal entities that are permitted under the Commercial Code include joint stock companies (anonim şirket), limited companies (limited şirket), collective companies (kollektif şirket), commandite companies (komandit şirket) and cooperative companies (kooperatif şirket). Non-incorporated enterprises (adi ortaklık) do not have legal personality and are regulated under the Code of Obligations.

Domestic and foreign investors commonly choose to form joint stock companies or limited companies as these entities have a number of features that are useful for doing business in Türkiye. Joint stock companies are the most sophisticated type of entity and are mandatory in certain regulated sectors such as banking, factoring, insurance, asset management and independent auditing.

The table below presents a comparison between the main features of joint stock companies and limited companies:

| Joint Stock Company | Limited Company | |

| Number of shareholders | Minimum one shareholderNo restriction on the maximum number ofshareholders | Minimum one shareholderMaximum number of shareholders limited to 50 |

| Minimum capital | Minimum required share capital is ₺250,000 (or ₺500,000 for companies under the “authorized capital” regime) | Minimum required share capital is ₺50,000 |

| Nominal share value | Nominal value of each share must be ₺0.01 or a multiple of that amount | Nominal value of each share must be ₺25 or amultiple of that amount |

| Authorized non-issued capital | May have authorized non-issued capital | May not have authorized non-issued capital |

| Public trading | May be publicly traded | May not be publicly traded |

| Regulated industries | Certain regulated industries require joint stock companies | Certain regulated industries do not permit limited companies |

| Debt instruments | May issue debt instruments | May not issue debt instruments |

| Financial assistance | There are certain prohibitions on financialassistance to fund the acquisition of a joint stock company’s own shares | There are no prohibitions on financial assistance tofund the acquisition of a limited company’s ownshares |

| Shareholder liability | Shareholders may not be held responsible forpublic debt of the company | Shareholders may be held responsible for publicdebt of the company |

| Share transfers | Share transfers are not, as a general rule, subject to any restrictions. Share transfers may be restricted, to a certain extent, by shareholders in the Articles of Association. | Share transfers are subject to the approval of the General Assembly. Approval may be withheld for any reason without providing justification. Share transfer agreements must be notarized and registered with the Trade Registry. |

Foreign companies may establish branches or liaison offices while Turkish companies may establish branches. Branches are registered with the trade registry, do not have separate legal personality and are not completely independent from the head office. Branch office activities must be in line with the head office’s activities.

Liaison offices differ from the structures described above in that they may not engage in any commercial activity and therefore may not generate any income or incur any losses. As the restriction on “not engaging in commercial activities” is interpreted strictly by the supervisory authorities, the activities of liaison offices are generally limited to gathering market information. Foreign investors often use liaison offices to familiarize themselves with the Turkish market prior to starting operations. Liaison offices are subject to permits which are issued for initial periods of up to three years and may be extended thereafter. The Ministry of Industry regulates liaison offices, and the representative offices of foreign banks are subject to oversight by the BDDK.

Each company is registered with the trade registry in the city where its headquarters are located. In addition, each branch of each company is also registered with the trade registry in the city where the branch is located. If all of the required documentation is available and in compliance with the formal requirements, establishment of a company or branch office should not take more than a few business days. The documents requested by trade registries are standard but can change from time to time, and documents in a foreign language must be certified and translated according to specific procedures.

Joint Stock Companies

A joint stock company is a corporation with a minimum capital of ₺250,000 represented by shares and has legal personality. Sole-shareholder joint stock companies are also permitted.

As a general rule, no governmental consent or approval is required to set up a joint stock company. Registration with the relevant trade registry and notification to the Ministry of Industry for foreign investors are sufficient. However, establishment of a company that will operate in a regulated sector requires, among other regulatory approvals, the prior consent of the Ministry of Trade.

The articles of association (ana sözleşme or esas sözleşme) is the main constitutive document for this type of legal structure. The articles of association specify the name, headquarters, purpose, share capital amount, type of company shares (registered or bearer), number of directors and other information concerning the company. It is filed with the relevant trade registry and announced publicly in the Trade Registry Gazette. The articles of association are binding on every shareholder of a joint stock company.

Certain matters, including increases or decreases of share capital, are exclusively reserved for decisions by the general assembly of shareholders. The articles of association must be amended to reflect any changes to the share capital.

The Commercial Code permits an “authorized capital” system for joint stock companies. Under this system, the shareholders determine a ceiling amount of authorized capital in the articles of association. The board of directors may then increase the company’s share capital by issuing new capital up to such ceiling during a period of five years without further general assembly approval for each increase. Currently, the statutory minimum share capital amount under the authorized capital system is ₺500,000.

Public companies may also operate under the authorized capital system after seeking the approval of the Capital Markets Board.

Capital may be cash or non-cash. Any non-cash capital must be transferrable and not encumbered. Non-cash capital must be valued by an expert appointed by the relevant commercial court. Personal services, receivables not yet due or commercial reputation may not be contributed as capital.

Mandatory Corporate Bodies of Joint Stock Companies

Board of Directors

A joint stock company is managed and represented by its board of directors. The board may be composed of one or more directors who may be individuals or legal entities. Directors are elected by the general assembly for a maximum term of three years and may be re-elected. Directors need not be shareholders of the company. Legal entity directors must appoint an individual representative to take the necessary corporate actions on their behalf. There are no citizenship or residency requirements for serving as a director. Certain share classes or minority shareholders (please see “Minority Rights” subsection of this chapter for further information on minority shareholders) may be given the privilege to appoint a specific number of members to the board. The board may hold physical or electronic meetings and pass resolutions by written consent in lieu of a meeting. While the Commercial Code sets forth the minimum meeting and decision quorums, a higher number may be specified in the articles of association. Although the board may delegate certain of its powers to one or more directors or officers, at least one board member must maintain the power to represent and bind the company.

General Assembly of Shareholders

Certain matters are exclusively reserved for decision by the general assembly of shareholders. Such matters include amendments to the articles of association, changes to share capital and the election or removal of directors. The general assembly must convene annually on an ordinary basis and may convene as needed on an extraordinary basis. While the Commercial Code sets forth the minimum meeting and decision quorums, the articles of association may specify a higher number. Each shareholder has the right during the general assembly to ask questions to the directors and auditors and to request a special audit on a specific matter.

Shares of Joint Stock Companies

A joint stock company requires a minimum capital of ₺250,000 with each share having a nominal value of ₺0.01 (one kuruş) or a multiple of that amount. 25 percent of the share capital of a joint stock company must be paid in before registration and the remaining 75 percent must be paid in within two years following registration.

Shares may not be issued for a value lower than the nominal value. However, shares may be issued with a premium in excess of the nominal value. Any such excess over the nominal value is transferred to the company’s reserves.

Preferred or preference shares are defined in the Commercial Code as privileged shares (imtiyazlı pay). Privileged shares may be issued if permitted in the articles of association. With the exception of the privilege to appoint members to the board of directors, privileges such as dividend or voting privileges are attached to the share and not to the person holding the share.

Shares may be in either registered form (nama yazılı) or bearer form (hamiline yazılı). While it is not mandatory to issue certificates to represent registered shares, doing so may be convenient for certain share transactions such as transfers or pledges. Minority shareholders have a right to request the issuance and delivery of certificates representing registered shares. Such share certificates must then be delivered to all shareholders.

Uncertificated registered shares may be transferred with a written transfer agreement. If certificated, shares are transferred by delivering the share certificate. In addition, for registered share certificates, it is required that the transferor duly endorses the back of the certificate. Transfer of bearer shares requires notification and registration with the Central Registry Agency (Merkezi Kayıt Kuruluşu).

Shareholders have statutory pre-emptive rights to participate in capital increases in proportion to their shareholding. This right may only be restricted or revoked for justified reasons by a general assembly resolution approved by shareholders holding at least 60 percent of the share capital.

As a general rule, registered shares that are fully paid-up may, subject to any specific restrictions in the articles of association, be freely transferred. Restrictions requiring the company’s approval for transfer must be based on justifiable grounds relating to the composition of shareholders, the business of the company, the economic independence of the company or sector-specific regulations. For example, share transfers in companies operating in regulated sectors (for example, power, banking, insurance and financial services) may be subject to the relevant regulatory body’s approval, if the transfer exceeds certain thresholds.

Registered shares that are not totally paid-up may only be transferred with the company’s approval, unless the transfer is due to inheritance, a marital property regime or enforcement of an obligation. The company may refrain from giving its approval only if the transferee does not have the ability to pay for the shares.

Please see “Security and Collateral” under “Banking and Finance” for details on share pledges.

Joint stock companies may purchase their own shares up to a value equal to 10 percent of the share capital, subject to conditions stipulated by the Commercial Code.

Although the Commercial Code expressly permits shareholders in a limited company to include in the articles of association rights of first refusal, call options and put options (in which case these rights are enforceable against third parties), there is no equivalent permission for joint stock companies. In practice, however, such rights and options are often included in shareholders’ agreements and sometimes in articles of association of joint stock companies. Because the elements of shareholders’ agreements are not specifically defined in the law, and also because a shareholders’ agreement may not override the articles of association, the enforceability of these provisions is questionable and remains a topic of discussion in Turkish law. Moreover, the limited enforceability of specific performance clauses (requiring a party to perform a contractual obligation as set forth under the contract) under Turkish law further complicates the enforceability of shareholders’ agreements in practice. Therefore, remedies for breach are not enforceable against third parties and remain at the contractual level among the shareholders.

Dividends of Joint Stock Companies

Dividends may only be distributed out of net profits and legal reserves. Before distribution of dividends, the Commercial Code requires an allocation equal to 5 percent of profits (before taxes and previous years’ losses) to statutory legal reserves. This allocation is not required if accumulated reserves exceed 20 percent of the paid-in capital. Additional voluntary contributions to reserves are permitted. A dividend equal to 5 percent of the company’s paid-in capital may be distributed to shareholders from net profits. The dividend distribution percentage may be higher if stipulated in the articles of association.

Advance dividend distributions are permitted if the company has generated profits and the general assembly has resolved to do so in advance. For public companies, specific authorization to make advance dividend distributions must be permitted in the articles of association.

Financial Assistance Prohibition

The Commercial Code prohibits joint stock companies from granting loans or security or to advance funds for the acquisition of their own shares. A target company may not (i) grant any loan, (ii) advance any funds or (iii) provide its own assets as collateral for an acquisition financing. However, shares of the target company owned by the shareholders, not the company, may be provided as collateral.

The Commercial Code provides for two exceptions of limited application to this prohibition. The first relates to transactions by banks or other financial institutions and is limited to scenarios where the bank or financial institution is the target company. The second exception is for transactions involving the purchase of a company’s shares by the employees of the company or its subsidiaries.

Limited Companies

A limited company must have a minimum capital of ₺50,000 with each share having a nominal value of ₺25 or a multiple of that amount. Shares may be certificated or uncertificated.

Limited companies are not allowed to undertake certain regulated activities, such as banking and insurance, and may not be publicly listed. As with joint stock companies, the articles of association of a limited company must contain certain required information and must be registered for public disclosure with the Trade Registry.

One of the distinct characteristics of limited companies is that although the liability of the shareholders is limited to their share capital, shareholders may be held personally liable for the public debts, such as taxes and social security payments, of the company. It is also possible in the articles of association to stipulate that shareholders may have additional liabilities such as capital contribution requirements.

Mandatory Corporate Bodies of Limited Companies

Manager(s)

A limited company must be managed and represented by at least one manager. Managers may be selected from third parties; however, it is required that at least one shareholder have the authority to represent and bind the company. Managers may be individuals or legal entities. Legal entity managers must appoint an individual representative to take the necessary corporate actions on their behalf. There are no citizenship or residence requirements for managers.

General Assembly of Shareholders

As with joint stock companies, the general assembly of shareholders is the other mandatory corporate body in a limited company. The Commercial Code reserves certain matters, such as amendments to the articles of association, appointment or removal of managers and approval of share transfers, exclusively for the general assembly.

Shares of Limited Companies

Share transfer agreements must be in writing and certified by a Turkish notary public. Unless otherwise stipulated in the articles of association, the general assembly of shareholders must approve share transfers. The articles of association may prohibit share transfers altogether. If the general assembly of shareholders does not approve a share transfer or share transfers are prohibited under the articles of association, a shareholder may withdraw from the company and ask to be paid the fair market value of the shares held by such shareholder by initiating a lawsuit against the company. Limited company share transfers must be registered with the Trade Registry.

The articles of association may give shareholders or the company itself rights of first refusal or call and put options.

Non-Incorporated Enterprises

Under the Code of Obligations, individuals or legal entities may form non-incorporated enterprises. Because such enterprises do not have legal personality, they are sometimes preferred for projects undertaken by partners where the corporate formalities of a legal entity are not necessary. For example, a joint venture may be formed for a specific purpose such as bidding in a tender.

At the heart of the non-incorporated enterprise lies a contractual relationship between at least two persons. Each partner must contribute a partnership interest, which may be of an intangible nature, such as physical or intellectual efforts, goodwill and know-how. Third parties may also be appointed to represent or manage the non-incorporated enterprise.

Partners are personally responsible for the debts of the partnership. Unless otherwise determined by all partners, each partner has the right to individually represent and bind the partnership, and each partner may oppose and prevent an action taken individually by another partner prior to completion of such action.

Other Forms of Legal Entities

Less common forms of corporate entities are collective companies, commandite companies and cooperative companies. These types of companies establish a more informal relationship between the shareholders. In the case of collective companies, all shareholders, and in the case of commandite companies one class of shareholders, may be held personally liable for all of the company’s debts and obligations. Cooperative companies are legal entities established for cooperative supply of various needs related to the founders’ professions, crafts and other businesses. Cooperative companies are based on the principle of mutual help and collaboration.

The Turkish legal system permits two types of non-profit legal entities, namely associations and foundations. Associations are entities formed without any capital requirement and require at least seven members to exist. There is no citizenship requirement for members of associations; however, a member who is not a Turkish citizen must be legally residing in Türkiye. Foundations must be not-for-profit, have at least one real or legal person member and require the allocation of real estate, a regular income or a lump sum capital to the fulfillment of its stated activity or purpose. There must always be a sufficient amount of funds remaining to fulfill the goal of the foundation and provide continuity. If the funds are consumed, the foundation is terminated by the state.

Governmental agencies monitor the operations of non-profit entities principally to check whether resources are correctly used for the charitable purposes indicated in their constitutional documents. Accepting funds and donations and obtaining tax-exempt status for the entity and donor are subject to additional rules after the entity is formed. For example, an association seeking to raise funds from the general public must secure approval from the relevant governorship of the city where the fundraising activities will be undertaken. If these activities span several cities or the whole country, the association must secure the approval of the governorship under whose jurisdiction it resides. Neither type of non-profit entity may distribute funds to its members.

B. Fiduciary Duties

Joint stock company directors and limited company managers must perform the fiduciary duties of loyalty and care towards the company’s shareholders. The duty of loyalty stems from the mandate given to directors and managers by the shareholders to manage the company. As an extension of this duty, directors and managers are not allowed to enter into transactions with the company itself or enter into competition with the company without the approval of the general assembly. In respect of the duty of care, directors and any person with delegated board powers are required to carry out their duties diligently. Failure to act in accordance with objective standards required from such position for exercising the duty of loyalty and care may result in being held liable for breaching this duty.

While fiduciary duties have traditionally been a concept applicable to directors and managers, the Commercial Code has introduced the principle of expanding fiduciary duties to shareholders who are in control of a “group of companies.” This concept is important since conglomerate structures are a common feature of the Turkish economy. Foreign investors can easily find themselves in control of a “group of companies” and therefore subject to fiduciary duties.

A corporate “group of companies” is deemed to exist if there is a structure of at least one parent company and two subsidiaries controlled by that parent company. This structure is applicable to both joint stock and limited companies. It is sufficient for any one of these companies to be headquartered in Türkiye. In corporate groups, the parent company has a fiduciary duty of loyalty to each subsidiary and may not impose a transaction on the subsidiaries that would cause harm to one subsidiary to the benefit of the other. In such case, the parent must compensate the harm within a certain amount of time. Failure to do so may result in a shareholder or creditor of the aggrieved subsidiary filing for damages against the parent (as well as the parent’s shareholders and directors) and requesting compensation.

In addition, if the shareholding percentage of an entity in a joint stock company or limited company exceeds or goes below defined thresholds (5 percent, 10 percent, 20 percent, 25 percent, 33 percent, 50 percent, 67 percent or 100 percent), such shareholder (whether or not it is controlling) is required to make disclosures to the company, the Trade Registry and, if the company is regulated, to any relevant regulatory bodies. Failure to make the disclosure results in the suspension of important shareholder rights including voting and dividend rights.

The board of directors has special responsibilities in cases of capital loss (sermaye kaybı) and significant debt (borca batıklık).

The Commercial Code regulates two scenarios of capital loss. First, if it is understood from the most recent year’s financial statements that half of the company’s share capital and legal reserves have been lost, the board of directors must immediately call a general assembly meeting and propose a corrective action plan to the shareholders. Second, if the most recent year’s financial statements reveal that two-thirds of the company’s share capital and legal reserves have been lost, the board of directors must immediately call a general assembly meeting. Unless the general assembly decides (i) to accept the loss and resume operations with only one-third of the capital by way of capital decrease or (ii) compensate the loss by injecting capital, the company is automatically dissolved without any legal proceeding or action. All interested parties may ask the courts to issue a declaratory ruling to this effect.

If there are signs that the company is in significant debt, the board of directors is responsible for preparing an interim financial statement. If the interim statement reveals that the company’s assets (excluding those without which the company cannot continue to operate), if sold, would still be unable to pay its debts, the board of directors must notify the competent commercial court. This notification would constitute a bankruptcy filing.

The managers of limited companies have the same responsibilities in the event of capital loss or significant debt of a limited company.

C. Accounting and Audit

Private joint stock companies and limited companies that meet certain criteria (for example, net asset, net sales revenue and number of employees) and all public companies regardless of these criteria are subject to independent audit. In addition, all companies operating in regulated sectors (such as banking, capital markets and telecommunications) are also subject to independent audit requirements.

In an effort to align the accounting practices with internationally recognized rules, the Commercial Code requires financial statements to be prepared in accordance with the Turkish Accounting Standards and Turkish Financial Reporting Standards that are in line with IFRS. In 2015, in an effort to establish compliance with IFRS to the greatest extent possible, a conceptual framework for financial reporting including a set of reporting standards and interpretation guidelines was published in the Official Gazette. These standards are continuously updated in accordance with the amendments made by the International Accounting Standards Board.

There are also related disclosure and reporting obligations for companies deemed to be part of a “group” (as defined in Section II. B above). The board of directors of subsidiary entities are required to prepare an annual report setting out all transactions within the corporate group. The report must specify any losses suffered and, if applicable, whether those losses have been compensated for within the group.

D. Minority Rights

Shareholders holding at least 10 percent of the capital in privately held joint stock or limited companies or at least 5 percent of the capital in public companies have certain statutory rights. These rights include affirmative rights to take certain actions and veto rights to block certain actions proposed by other shareholders. The articles of association may provide a lower shareholding threshold than what is required by statute.

Minority shareholders may request:

- Issuance of registered share certificates;

- The board of directors to convene a general assembly and adding items to the meeting agenda;

- Adjournment of balance sheet discussions for a month;

- Dissolution of the company on just grounds;

- Information from the board of directors or auditors at a general assembly meeting. Any shareholder, regardless of the statutory minority threshold, may request information; and

- Appointment of a special auditor on certain issues. Again, any shareholder, regardless of the statutory minority threshold, may request this.

The resolutions listed below require approval, by law, of a specific supermajority of the shareholders and therefore may be blocked by minority shareholders holding sufficient capital to preclude such a supermajority. The statutory supermajority requirements may be increased under the articles of association (unless, of course, it is 100 percent). Requirements other than the approval of a specified majority of share capital may also apply in order to take the actions listed below.

| Resolution | Minimum Vote Required |

| Imposing monetary obligations to cover balance sheet losses | 100% of the share capital |

| Changing the nationality of the company | 100% of the share capital |

| Minority squeeze out | 90% of the share capital |

| Changing the field of activity | 75% of the share capital |

| Issuing privileged shares | 75% of the share capital |

| Restricting transfer of registered shares | 75% of the share capital |

| Decrease of share capital | 75% of the share capital |

| Limiting or removing statutory pre-emptive rights | 60% of the share capital |

Shareholders may be squeezed out from a company in two circumstances: (i) merger and (ii) disruptive actions by minority shareholders in a corporate group.

In a merger scenario, shareholders owning 90 percent or more of the dissolving company may squeeze out minority shareholders by offering them the real value of their shares.

In a “group” of companies, the controlling company holding at least 90 percent of the shares of a subsidiary may squeeze out the minority shareholders if these shareholders act in bad faith and disrupt the business operations.

E. Termination

A company may be terminated voluntarily upon the decision of its shareholders or if certain specific circumstances exist, such as bankruptcy, expiration of a definite term, realization of a specified purpose or occurrence of a specific termination cause set out in the articles of association. If the articles of association of a company have a provision setting a certain date for termination, the company must be terminated at this date, although such provisions are not common in practice. Continuation of a company’s business activities after the expiration of the definite term tacitly deems it a company with indefinite period.

The owners of a company may, in a shareholders’ general assembly meeting where at least 75 percent of the total share capital is represented, approve voluntary termination.

Termination by court order is an extreme measure which is generally granted by Turkish courts only as a last resort. Courts look for one of the following causes before ordering termination:

Failed Company Management

Shareholders may file a lawsuit for the company’s termination (i) if the general assembly of shareholders cannot convene at least once a year on an ordinary basis or on an extraordinary basis whenever necessary or (ii) in the absence of statutory corporate bodies (notably the board of directors). Depending on the specifics of the case, absence of the board could occur if the term of the board expires and a new board is not elected, if the members of the board resign and no new members are appointed or if the members of the board fail to convene at all or as required. Creditors of a company or the Ministry of Trade may also file a lawsuit to terminate a company for failed management.

Other Just Causes

Shareholders collectively representing a minimum of 10 percent of the company’s share capital (or lower percentage if provided for in the articles of association) may file a lawsuit for the termination of the company in the event of just causes. “Just causes” are not defined in the Commercial Code and are considered by courts on a case-by-case basis.

III. PROTECTION OF FOREIGN INVESTMENTS

Foreign investments are protected by the Constitution, the Foreign Direct Investment Law and other related regulations. In the international context, Türkiye is party to 117 bilateral investment treaties on the protection and promotion of investments, 69 of which are currently in force, and 91 double taxation treaties, as well as several treaties regarding customs union, free trade, multilateral investments, protection of social security rights and agreements concerning alternative dispute resolution methods. The Foreign Direct Investment Law seeks to: (i) regulate the principles promoting foreign direct investment, (ii) protect the rights of foreign investors, (iii) standardize definitions of investment and investor, (iv) establish a notification-based system for foreign direct investment and (v) increase foreign direct investment.

The Investment Office of the Presidency and the Coordination Council for the Improvement of Investment Environment are the two major institutions that promote inbound foreign investment.

A. Domestic Legislation on Foreign Investment

With the exception of certain limited areas, described in more detail below, foreign investors are on an equal footing with Turkish investors.

The applicable legislation defines “foreign investor” as a foreign individual, foreign entity or non-resident Turkish citizen making a foreign direct investment into Türkiye. “Foreign direct investment” includes assets of foreign or domestic origin that are used to establish a new company or branch or to acquire shareholding in a Turkish company. Assets of foreign sources may include cash capital, corporate securities (excluding government bonds), machinery, equipment or intellectual property. Assets of domestic origin may include profits, receivables or natural resource exploration rights.

Below are some of the exceptions to the equality principle between foreign and domestic investors:

- Foreign ownership in a media company may not exceed 50 percent.

- Certain maritime activities (for example, the transportation of passengers and cargo between Turkish ports) are reserved for Turkish individuals and entities.

- There are certain restrictions on real estate acquisition by foreign individuals or entities and Turkish companies with foreign capital. Please see “Property Rights” for further details.

- Certain professions, such as the practice of law or medicine, have restrictions for non-Turkish individuals or entities. In addition, the issuance of work permits for foreign employees in any sector is subject to certain conditions. Please see “Labor Law” for further details.

- Foreign real and legal persons may only fund or participate in private, secondary education institutions in which non-Turkish citizen students are enrolled; they may not establish or participate in higher education institutions.

- Other areas stipulated by international agreements or other relevant special laws may not be open to investment by foreign individuals or entities.

Subject to the above, domestic legislation provides the following minimum standards of protection to foreign investors:

Equal Treatment with Domestic Investors

Foreign investors may not be subject to a more burdensome treatment than a Turkish national merely due to their nationality.

Expropriation and Nationalization

Assets and enterprises owned by a foreign or domestic investor may not be expropriated or nationalized without due process or just compensation.

Expropriation and nationalization may only take place if required by the “public interest” as determined by the relevant administrative body. The applicable administrative body would depend on the nature and scale of the investment and may include the board of governors of a city or province, a ministry or the Office of the President. The decision of an administrative body is subject to judicial review.

Following an expropriation decision, the administrative body and the owner of the property may agree on the amount of compensation. Failing such agreement, the Civil Court of First Instance determines the value of expropriated assets and the terms of payment.

Expatriation of Proceeds

Investors are allowed to transfer proceeds from operations and transactions in Türkiye abroad (including net profits, dividends, returns from sales, liquidation payments, compensation payments and any amounts payable in return of a management agreement, as well as capital and interest payments of loans) through banks or financial institutions.

Dispute Settlement

The Foreign Direct Investment Law stipulates different methods for handling disputes based upon the type of investment. Disputes arising from investment agreements are subject to private law. Disputes arising from investments made relating to public service concessions contracts or concluded with foreign investors may either be handled by authorized local courts or referred to national or international arbitration or other means of dispute settlement. It is important to note, however, that venue choice for dispute resolution for public concessions contracts and investments with foreign investors is only possible in circumstances where all conditions in the related regulations are fulfilled and agreed upon in advance by the parties involved.

Valuation of Capital in Kind and Foreign Securities

Capital in kind is valued within the regulations of the Commercial Code. When securities are used by foreign investors as an investment tool, the value of the security shall be considered to be the value determined by the relevant authorities in the country of the asset’s origin.

Obligations of Foreign Investors under the Foreign Direct Investment Legislation

Foreign investors having a subsidiary, branch or liaison office in Türkiye have certain notification obligations. For instance, companies and branches must notify the Ministry of Industry through an online platform, the Electronic Incentive Application and Foreign Investment Information System (E-TUYS) about any changes in foreign ownership in their share capital. This notification requirement is generally included as a post-closing item in mergers and acquisitions transactions.

Liaison offices are under a similar obligation to notify their activities and are also subject to audits by the Ministry of Industry to determine if their activities are in compliance with their permit and applicable legislation. Please see Section II. A “Corporate Structures” under “Corporate Environment” for details on liaison offices.

B. International Treaties

Türkiye is party to several international treaties for the protection and promotion of foreign investment. These international treaties have the force of law once they are ratified by the Parliament. Türkiye is a party to 137 bilateral investment treaties, of which 83 are currently in force. The contracting parties include all the EU member states except Ireland, as well as all the OECD member countries except Iceland, Canada, Norway and New Zealand. Türkiye is also party to numerous double taxation treaties.

Türkiye’s bilateral investment treaty and double taxation treaty counterparts include almost all OECD and European Union countries, including the United States, Russia, China, Germany and the United Kingdom.

Bilateral investment treaties provide certain investment protections to foreign investors that are above and beyond the protections already provided under domestic law and the structuring of transactions from a treaty protection perspective has become a more commonly used method in recent years.

Türkiye does not have a standard bilateral investment treaty template; therefore specific provisions vary depending on a treaty’s counterparty nation. However, the substantive investment protection rights typically granted are as follows:

- International Arbitration: The host country consents to dispute resolution by international arbitration so that the foreign investors are not obligated to legal recourse in the host country’s local courts.

- Most-Favored-Nation: Provides treatment to all foreign investors no less favorable than the best treatment that the host state accords to any foreign investor under a bilateral investment treaty, in effect expanding the scope of bilateral protection to include the rights negotiated by other most-favored-nations.

- National Treatment: Provides foreign investors with treatment no less favorable than the host state provides to investors of its own state.

- Expropriation: The host state guarantees to provide the investor with the full and fair value of an expropriated investment.

- Expatriation of Profits: The host state guarantees that the investor may freely transfer its profits, dividends and compensation payments overseas through banks.

- Fair and Equitable Treatment: The host state has an obligation to offer a stable and predictable legal framework, due process, transparency and consistency without discrimination.

- Full Protection and Security: The host state has an obligation to prevent physical destruction of the investment.

- Other than bilateral treaties, Türkiye is party to a number of multilateral investment agreements including the following:

- ICSID Convention: In force since 1966 and ratified by 165 states, this convention permits settlement of certain investment disputes through arbitration administered by ICSID, an institution organized under the World Bank Group. Either the investment contract or the underlying investment treaty must provide for ICSID jurisdiction in order for investors to use this recourse.

- The Energy Charter Treaty: In force since 1998 and ratified by 49 states (although some states have declared their intention to withdraw from the treaty), the European Union and the Euratom, the treaty provides for inter-governmental cooperation and substantive protection of foreign investments (similar to those protections described under bilateral investment treaties) in the energy sector.

- Organisation of Islamic Cooperation Investment Treaty: In force since 1988, it provides for principles for the promotion of capital transfers among 56 member states as well as the protection of investments.

C. International Dispute Resolution

Alternative Dispute Resolution for International Investment Disputes

Bilateral investment treaties give foreign investors the option of recourse to Turkish local courts or international arbitration. They often include an option to arbitrate under the ICSID Convention. However, arbitration under the UNCITRAL Rules or the ICC Rules of Arbitration are also commonly used. According to ICSID data, Türkiye is mainly a party to investment-related disputes concerning the energy, telecommunications and construction sectors.

The ICSID Convention also provides a specific mechanism for the enforcement of arbitral awards. Under the ICSID Convention, member states must recognize an ICSID award as binding and enforce the award’s monetary obligations as if it were a final judgment of a court in that state. The Energy Charter Treaty also provides specific rules for enforcement.

Enforcement of an Arbitral Award or a Foreign Court Judgment

Türkiye is party to the New York Convention, which requires domestic recognition and enforcement of foreign arbitral awards. Türkiye has made two reservations to the applicability of the New York Convention: (i) the award should be given in a member state and (ii) the subject matter of the dispute should be, as interpreted under Turkish law, of a commercial nature.

Türkiye also has its own domestic law, namely the International Private and Procedure Law, that governs the enforcement of foreign arbitral awards and foreign court decisions.

Both the New York Convention and the International Private and Procedure Law excuse enforcement in cases involving invalid arbitration agreements, violations of due process rights or excess of authority by the arbitral tribunal or of the scope of the arbitration agreement.

It is important to note that Turkish courts do not re-evaluate a dispute subject to the final judgement of foreign courts based on merit. Turkish courts only examine whether the foreign court’s judgement meets the recognition and enforcement requirements specified under Turkish law. This rule, known as prohibition of revision, is also stated in the precedent judgements of the General Assembly of the Supreme Court of Appeal on the Unification of the Judgments.

In addition, both pieces of legislation excuse enforcement if enforcement of arbitral awards and foreign court judgments would violate the “public policy” of Türkiye. The concept of public policy is not expressly defined and is left for interpretation by courts in line with, but without being bound by, Supreme Court of Appeals precedents. In general, constitutional rights, fundamental legal principles, international legal instruments pertaining to basic rights, commonly accepted ethical values, the standard of honesty and good faith and public health and safety are considered to be public interest matters. The Supreme Court of Appeals in past decisions has also interpreted customs and tax laws as being part of public policy.

Final judgments of foreign courts regarding private law matters may be enforced or recognized by Turkish Courts of First Instance in accordance with the provisions of the International Private and Procedure Law. Turkish law requires (i) reciprocity between Türkiye and the state where such decision was taken, arising from a law, bilateral agreement or court practices, (ii) that the judgment does not relate to any matter that falls within the exclusive jurisdiction of Turkish courts (for example, a matter relating to the ownership of property located in Türkiye) and (iii) that due process has been observed and enforcement would not violate public policy.

D. Istanbul Arbitration Centre (ISTAC)

Fully operational since 2016, ISTAC was established to make Istanbul an arbitration hub in the MENA and CEE regions.

With rules comparable to internationally-accepted arbitration platforms such as the ICC, ISTAC offers dispute resolution services to all contracting parties, including for disputes involving a “foreign element,” without any membership requirements. Unless otherwise selected by the contracting parties, the seat of arbitration under ISTAC rules is Istanbul.

Parties may also select the language for arbitration and determine the number of the arbitrators. ISTAC rules provide for “fast track” arbitration, which enables the issuance of an award within three months by a single arbitrator. They also allow for an “emergency arbitrator” concept, designed for parties in need of urgent interim measures that cannot await the arbitrator(s) to take office.

ISTAC published rules governing “Mediation-Arbitration” (Med-Arb), an alternative dispute resolution procedure with the characteristics of both mediation and arbitration, on its website in November 2019.

Additionally, since April 2020, it has been possible to conduct an ISTAC Rules arbitration proceeding without the requirement of physical attendance. Hearings are conducted through teleconference or video conference and are subject to the rules and principles outlined in ISTAC’s Online Hearing Rules and Procedures.

The Swiss Arbitration Association (ASA) and Istanbul Arbitration Center signed a cooperation protocol in July 2022. In 2017, ISTAC also signed a cooperation agreement with the Permanent Court of Arbitration (PCA), based in The Hague. In addition, Istanbul Arbitration Center signed cooperation protocols with Qatar International Center for Arbitration (QICCA) in 2018, Kyrgyzstan Arbitration Center in 2019 and Hong Kong International Arbitration Center (HKIAC) in 2021.

IV. PROPERTY RIGHTS

The acquisition and ownership of movable and immovable property are governed by well-settled Turkish laws. In addition, Turkish law recognizes that a person may have certain benefits associated with immovable property without having the rights of ownership. These rights are generally referred to as “non-ownership rights” and are described in more detail below. The principal legislation relating to property rights is the Civil Code.

Rights relating to intellectual property are mainly protected under two different legal regimes: (i) copyright protection and (ii) protection of other registered rights such as trademarks, designs, utility models, patents and geographical indications. Copyright is protected under the Intellectual Property Law while trademarks, designs, utility models, patents and geographical indications are protected under the Industrial Property Law. The Turkish Patent and Trademark Office provides protection of registered rights. Legal disputes relating to intellectual property rights are resolved by specialized courts.

A. Acquisition of Title and Ownership Rights

Title to Movable Property

Title to movable property manifests itself through possession (that is, physical and actual control over the property). As a general principle, it is sufficient for the transfer of title that the power of control is given to the new owner and no registrations or formal requirements are sought. However, as an exception, a formal transfer process or registration may be required for certain types of movables. For instance, the transfer of certificated shares in a company requires an endorsement on the back of the certificate, and the sale of an automobile requires a deed executed before a notary public and registration with the motor vehicles registry.

Title to Immovable Property

State-Owned Property

Turkish law mandates that certain immovable property remains state-owned. All other immovable property may be privately-owned. Under Turkish law, there are two classes of state-owned property:

Non-Transferable State Property

This type of non-transferable property is under the control and at the disposal of the state and may be subject to certain non-ownership rights under exceptional cases regulated by law. Examples of non-transferable state property include: public water supply, land that is not cultivatable such as rocks, hills, mountains and glaciers and resources originating therefrom, coastlines, natural resources, petroleum sources and mines. Non-transferable state property may not be: (i) transferred, sold or acquired, (ii) subject to private-law arrangements that may result in the sale and transfer of title (for example, a mortgage) or (iii) subject to attachment proceedings (that is, the legal process of seizing a debtor’s property for the purpose of satisfying a claim that is due and unpaid). However, various pieces of legislation permit the use, generally for public interest, of such property by individuals and/or private legal entities.

Transferable State Property

This property is privately-owned by the state or by a state-owned enterprise and is freely transferable. Transferable state property includes the immovable properties acquired by the state through acquisition, expropriation, inheritance or donation. The state uses such property in the performance of public services or for commercial purposes to generate income. As such, the state may lease the property or operate the property itself or transfer it to third parties.

Foreign Ownership of Immovable Property

Immovable property may be acquired in the form of (i) land, (ii) independent rights registered with the title deed registry (such as servitude rights) or (iii) independent sections of a real property, such as flats, apartments, offices, shops and depots, subject to condominium rights (kat mülkiyeti). Acquisition of title to real property or a mortgage thereon requires an official transfer deed drawn up by the title deed officer or the notary public and registered with the title deed registry located where the real property is situated. Title deed registry records may be inspected by those persons who can establish a legitimate interest in the relevant property.

Foreign individuals are generally entitled to acquire and own immovable property in Türkiye. Foreign legal entities are entitled to acquire and own immovable property only in exceptional circumstances.

Acquisition by Foreign Individuals

Real property may be acquired subject to the following limitations:

- Individuals must be citizens of one of the white-list countries. Foreign individuals interested in acquiring real property in Türkiye may request information on these countries from Turkish embassies and consulates, the General Directorate of Land Registry and title deed offices.

- Ownership and servitude rights may not exceed, in aggregate, 30 hectares (74 acres) per individual.

- The total area of the real property acquired by foreign individuals in one district (ilçe) – an administrative sub-division of a province (il) – may not exceed 10 percent of the total area of privately held property in that district.

- Foreign individuals may not acquire real estate in military or security zones, which are designated by the Office of the President upon the General Staff’s recommendation and may include a certain perimeter around military establishments.

- Statutory restrictions do not apply to mortgages established in favor of foreign nationals. In case a mortgage is foreclosed, mortgagees (whether Turkish or foreign nationals) are entitled to the foreclosure proceeds but not the property itself. Please see “Enforcement of Security Interests” in “Banking and Finance” for more information.

Acquisition by foreign legal entities

- Real estate acquisition may only be done for the limited purposes set forth under the Petroleum Law, the Tourism Promotion Law and the Industrial Zones Law. There are no restrictions on the establishment of mortgages in favor of foreign companies. Foreign foundations or associations, on the other hand, are not allowed to acquire immovable property in Türkiye.

Acquisition by Turkish legal entities with foreign capital

- Turkish companies in which a foreign real person or legal entity holds 50 percent or more of the shares, either directly or indirectly, or has the right to appoint or remove the majority of directors may only own real property, mortgage rights or other servitude rights in order to conduct the activities listed in such company’s articles of association. The same restrictions apply if a company with foreign capital becomes a shareholder, directly or indirectly, in another Turkish company and the ultimate shareholding percentage of the foreign investor reaches or exceeds 50 percent. Acquisition or ownership of real property located in military or security zones by these companies is subject to permission.

B. Non-ownership Rights to Property

Under Turkish law, non-ownership rights are classified as either in rem rights enforceable against all persons (for example, servitude rights, pledges or impositions) or in personam rights enforceable against a contract counterparty (for example, a lease).

In Rem Rights

Rights in rem are property rights which may be asserted against third parties. Rights in rem over immovable property must be registered with the title deed registry. Provided that the rules of the foreign jurisdiction governing the acquisition of the in rem right are not against public policy in Türkiye, in rem rights created in accordance with the rules of any foreign jurisdiction over any movable property situated outside Türkiye are recognized by Turkish law when such movable property is brought into Türkiye. In addition, where Turkish law stipulates special conditions for validity in respect of the creation of such in rem rights, such as registration with a public registry, those conditions should be fulfilled in order to preserve the effectiveness of the in rem right within Türkiye.

Under Turkish law, partial ownership, whether by individuals or legal entities, may exist in two different forms: (i) ownership in common (paylı mülkiyet) where each owner has a distinct and proportionate interest in the whole property and (ii) joint ownership (elbirliği mülkiyeti) where each owner has an undivided interest in the whole property. Joint ownership exists only in a limited number of circumstances prescribed by law (for example, partners in a partnership). If the property is subject to ownership in common, then each owner has the right to dispose of its share of the property. If the property is subject to joint ownership, any disposition, including creation of a security interest, requires the unanimous consent of all joint-owners. Furthermore, property subject to joint ownership may only be mortgaged or pledged in its entirety and by all joint-owners at the same time.

Servitude Rights